Market Conditions Update - Spring 2026

Introduction - A Softer Winter with Stable Pricing

The Winter 2026 market in Victoria and the Gulf Islands was marked by softer sales activity, elevated inventory, and pricing that remained surprisingly resilient. Across December, January, and February, single-family home sales tracked below both the previous year and long-term seasonal norms, while active residential listings stayed well above typical levels. At the same time, average sale prices for single-family homes continued to edge upward, suggesting that while buyers had more choice and more negotiating leverage through the winter, well-positioned homes were still able to command strong values.

Sales Activity - Winter Demand Remained Subdued

Single-family home sales were subdued through most of the winter. In December, sales declined from the previous month and remained slightly below both the previous year and the 10-year average (down 22.8% month-over-month, 2.6% year-over-year, and 5.6% below the 10-year average). January softened further, with sales falling again from December and sitting more noticeably below both last year and seasonal norms (down 17.7% month-over-month, 21.1% year-over-year, and 15.7% below the 10-year average).

February brought a welcome monthly rebound, with sales rising from January (up 34.6% month-over-month), but activity still remained below both February 2025 and the longer-term average for the month (down 12.0% year-over-year and 20.1% below the 10-year average). In other words, demand improved as winter progressed, but not enough to suggest a full return to typical early-season momentum.

Overall, the pattern points to a market where buyers were still active, but many remained cautious. Affordability pressures, economic uncertainty, and a broader wait-and-see attitude appear to have kept some demand on the sidelines through the winter months.

Enlarge Graph

{kind=link}

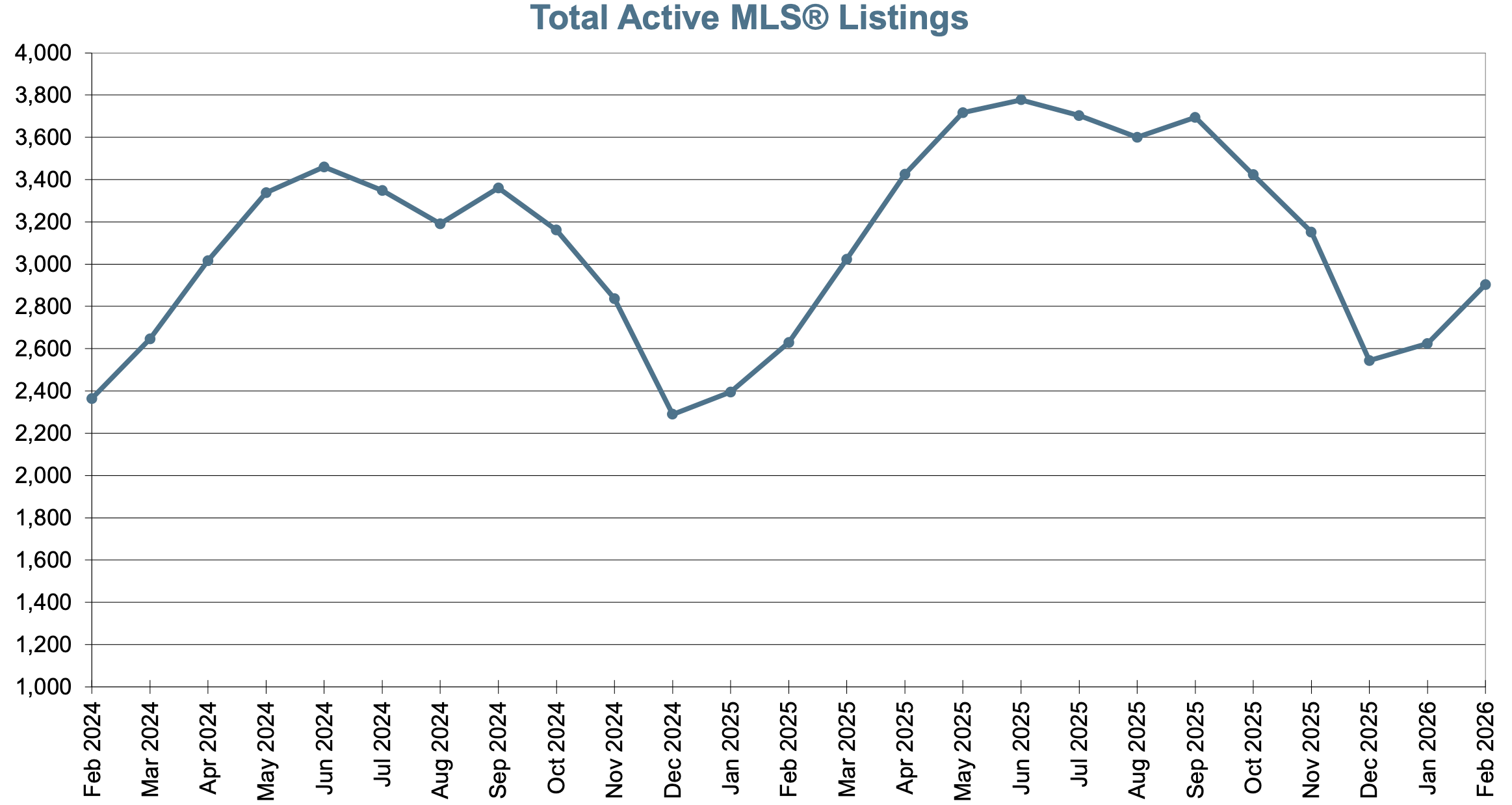

Listings Activity - Inventory Stayed Elevated

Active residential listings remained elevated throughout the winter and continued to give buyers more choice than they have had in many past years. December saw listings fall from November, which is normal seasonally, but inventory still sat above both the previous year and the 10-year average (down 23.0% month-over-month, up 10.3% year-over-year, and 47.1% above the 10-year average).

That elevated inventory carried into the new year. In January, listings increased from December and remained higher than both January 2025 and the long-term norm (up 5.7% month-over-month, 8.7% year-over-year, and 48.3% above the 10-year average). February continued that trend, with another notable monthly increase and inventory levels holding well above historical standards (up 13.7% month-over-month, 10.3% year-over-year, and 55.5% above the 10-year average).

This is one of the clearest themes of the season. Buyers had substantially more selection than is typical, and sellers faced a more competitive environment where listings needed to stand out. In a place like Salt Spring, where properties are highly varied and buyers often take time to weigh lifestyle fit as well as value, elevated inventory can make the market feel even slower and more discerning.

Enlarge Graph

{kind=link}

Market Conditions - Balanced Overall with a Brief Buyer Shift

The residential sales-to-active listings ratio showed a market that was largely balanced through the winter, with a brief dip into buyer-favourable conditions in January.

In December, the ratio was 19.1%, placing the market within the balanced range for Victoria and the Gulf Islands. January saw the ratio fall to 16.6%, briefly moving into buyer’s market territory, reflecting the seasonal slowdown in sales combined with elevated inventory. By February, the ratio recovered to 19.9%, returning the market to balanced conditions as sales activity picked up.

This pattern reinforces a key theme from the winter months. While buyers had increased choice and some negotiating leverage, the market did not shift into a sustained buyer’s market. Instead, it remained relatively stable overall, with short-term fluctuations driven by seasonal dynamics.

In practical terms, this meant that buyers had more room to negotiate than in recent years, particularly in January, but well-positioned properties were still attracting solid interest.

Enlarge Graph

{kind=link}

Prices - Values Continued to Edge Higher

Despite weaker sales activity and elevated inventory, average sale prices for single-family homes remained firm and rose through the winter. In December, the average sale price increased from November and sat modestly above December 2024 (up 4.7% month-over-month and 2.8% year-over-year). January saw prices rise again (up 1.7% month-over-month and 4.7% year-over-year). February continued the same pattern, with the average sale price increasing again from January and from the prior year (up 3.8% month-over-month and 5.4% year-over-year).

This is an important nuance in the Winter 2026 market. While activity was relatively soft and buyers had more leverage overall, prices did not weaken. That likely reflects the ongoing desirability of the region, the unique nature of Gulf Islands housing stock, and the fact that even in a slower market, quality properties continue to attract serious interest.

Looking at a longer time horizon, average prices are now roughly double what they were a decade ago. This reflects the strong long-term performance of real estate in the Gulf Islands and the sustained demand for lifestyle-driven markets like Salt Spring, even through periods of slower activity.

Enlarge Graph

{kind=link}

Looking Forward - A Measured Spring Could Build Momentum

As we move into Spring 2026, the outlook appears cautiously constructive. The Bank of Canada held its policy rate at 2.25% in March, noting that economic growth is being tempered by global uncertainty and risks. At the same time, Canada’s CPI inflation eased to 1.8% in February, although the Bank has warned that higher energy prices could push inflation up again in the coming months.

BCREA forecasts a 12.0% increase in BC home sales in 2026, with steady mortgage rates and pent-up demand supporting a gradual recovery. BCREA also notes that inventory remains near its highest level in over a decade and expects markets to remain balanced overall, which should help temper price growth even as sales improve.

Taken together, this suggests that Spring 2026 may bring somewhat more activity than we saw over the winter, but likely not a dramatic surge. A more probable outcome is a steady re-engagement of buyers, especially if confidence improves and borrowing conditions remain stable. For Salt Spring and the Gulf Islands, where purchasing decisions are often tied to bigger lifestyle moves, the spring market may build gradually rather than all at once

Opportunities for Buyers - Choice and Negotiating Room

For buyers, the current market offers meaningful opportunity. Inventory remains elevated, which means more choice, more time to evaluate options, and greater ability to negotiate on price, terms, and conditions. In a market where sales have been running below normal seasonal levels, buyers are often in a stronger position to act thoughtfully rather than react quickly.

This can be especially advantageous for buyers who are well prepared. Financing readiness, a clear understanding of priorities, and the ability to move decisively on the right property still matter. Even in a softer market, the most compelling homes can attract strong interest. But overall, Spring 2026 looks like a season in which buyers may be able to secure better value and better terms than they could in a more competitive environment

Opportunities for Sellers - Strategic Positioning

For sellers, the main opportunity in Spring 2026 is to stand out in a market where buyers have choice. That means thoughtful preparation and strategic pricing. Well-prepared and well-priced homes can perform strongly, especially as spring demand begins to build. Sellers who take the time to position their property properly are more likely to capture buyer attention early and sell quickly.

If you’re considering buying or selling, give me a call for expert advice and to begin exploring your options.

Gina Jacobsen, PhD

REALTOR®

(250)539-0828

gina@ginajacobsen.com

Sources:

Victoria Real Estate Board MLS® STATISTICS

British Columbia Real Estate Association Economics

Canadian Real Estate Association

Bank of Canada